Weekly Market Commentary December 28 2023

The Markets

Still exceeding expectations.

Last week, the United States Treasury market rallied. Yields fell and bond prices rose as some bond market investors enthusiastically embraced the idea that the Federal Reserve will soon change course. Michael Mackenzie and Rich Miller of Bloomberg explained:

“Softening inflation and employment data in the past month have convinced investors that the Federal Reserve is done raising interest rates and ignited bets that cuts of at least 1.25 percentage points are in store over the next 12 months. Treasury yields, which touched highs of 5% as recently as October, have declined sharply, with the U.S. 10-year benchmark sliding more than three-quarters of a percentage point.”

Bond investors were hoping that last week’s unemployment report would show jobs and wage growth slowing in November. Instead, employers added more jobs than expected (199,000 jobs vs. 180,000), and the unemployment rate fell to 3.7 percent.

On Friday, the Treasury market reversed course. Yields on long- and short-term Treasury bonds rose sharply and prices fell, reported Karishma Vanjani of Barron’s.

The employment report also showed that average hourly earnings increased in November – rising 4 percent year-over-year. Wages have risen faster than inflation for seven months, reported Sarah Foster of Bankrate. However, many workers are still feeling a pinch.

“While inflation has come down, broadly speaking, prices have not. There is a kind of continuing, virtual sticker shock that continues to weigh on the minds and pocketbooks of consumers that is meaningful,” according to Senior Bankrate Economic Analyst Mark Hamrick.

On the other hand, the unemployment rate in Canada rose to 5.8% in November 2023, up from 5.7% in October 2023, in line with market expectations. The count of individuals without employment rose by 11,000, reaching 1.24 million. Employment rose by 24,900 to 20.31 million, beating the 15,000 forecast, while the labour force increased by 36,000 to 21.55 million.

The average hourly wage of employees grew by 5.1% year-over-year in November, slightly lower than the 5.6% increase in October.

Inflation was 3.1% in October, above the Bank of Canada (BoC)'s 2% target for over two years. The BoC wanted core inflation to ease more and last longer. It said the economy was slowing and not overheating. High rates and low oil prices were hurting spending. The BoC was less concerned about inflation. It said many prices and core inflation were easing. The BoC told the market to be patient, as it did not agree with rate cut bets in early 2024. The BoC saw inflation around 3.5% until mid-2024, then 2% in late 2025. It believed the rate hikes were effective and enough.

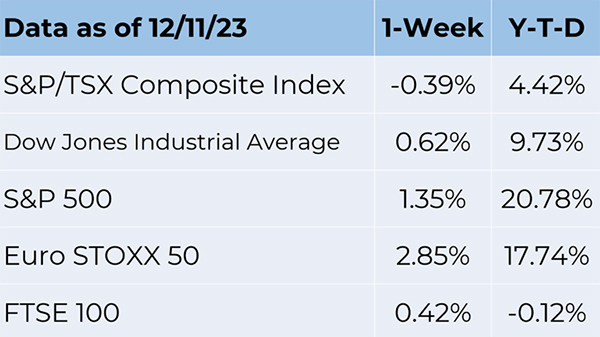

Last week, the Standard & Poor’s 500 Index gained for the sixth consecutive week, according to Bloomberg7 and yields on most maturities of U.S. Treasuries moved higher.

Source: FactSet

AMERICANS AGREE ON SOME THINGS. The Old-Age, Survivors and Disability Insurance (OASDI) program plays a significant role in the lives of many Americans. In 2022, it provided monthly benefits to 51 million retired workers and their dependents, 9 million disabled workers and their dependents, and the dependents of 6 million deceased workers.

In 2022, the program spent $1.24 trillion and took in $1.22 trillion. From here on out, the program’s spending is expected to exceed its funding. Under current assumptions, the trust fund will be depleted by 2034 – unless something changes.

An issue brief from the American Academy of Actuaries (AAoA) stated, “If Congress has not acted by 2034, we will be faced with an automatic 20% cut in benefits to people already receiving benefits, the need to immediately increase Social Security taxes by 25%, or some combination of cuts in benefits and increases in taxes.” The AAoA discussed options for keeping Social Security solvent, including:

- Increase the payroll tax rate by 25 percent. Currently, the payroll tax rate is 15.3 percent on up to $160,200 of a workers’ income. The worker pays half, and the employer pays half.This would cover 100 percent of the 2034 shortfall.

- Raise or eliminate the wage limit ($160,200 in 2023). This would cover 36 percent to 78 percent of the 2034 shortfall.

- Increase Social Security’s investment income by investing a portion of the money raised through taxes in equities.

- Tax Social Security benefits similarly to the way pensions are taxed. This would cover 8 percent of the 2034 shortfall.

- Reduce benefits for higher income recipients who are not yet eligible for benefits. This would cover 10 percent or less of the 2034 shortfall.

- Raise the retirement age for future recipients. If normal retirement age is raised to 69 by 2034, it would cover about 10 percent of the shortfall.

Many Americans are concerned about the future of Social Security. According to a survey conducted by Republican firm North Star Opinion Research, Democratic firm Global Strategy Group, and the nonpartisan Peter G. Peterson Foundation:

- 97 percent of Democratic participants and 97 percent of Republican participants want Congress to “reform Social Security and ensure it’s available for current retirees and younger generations.”

Weekly Focus – Think About It

"If it's your job to eat a frog, it's best to do it first thing in the morning. And if it's your job to eat two frogs, it's best to eat the biggest one first"

—Mark Twain, writer and humorist

Best regards,

Eric Muir

B.Comm (Hons. Finance), CIM®, FCSI

Senior Portfolio Manager

Derek Lacroix

BBA, CIM®, CFP®

Associate Portfolio Manager

Disclaimer:

Information in this article is from sources believed to be reliable, however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views are those of the author, Eric Muir and Derek Lacroix and not necessarily those of Raymond James Ltd. Investors considering any investment should consult with their Investment Advisor to ensure that it is suitable for the investor’s circumstances and risk tolerance before making any investment decision. Raymond James Ltd. is a Member Canadian Investor Protection Fund.